現在位置 : 房市 > 世界最大的樓市泡沫在哪?加拿大!

|

世界最大的樓市泡沫在哪?加拿大!

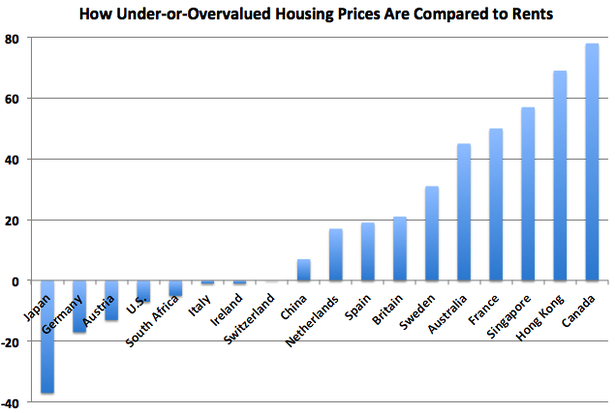

來源:新浪財經 Date: 2013-02-12 北京時間2月11日下午消息大西洋(10.20,0.02,0.20%)月刊目前報道房地產市場是否存在泡沫可能並非是只是簡單的主觀判斷,與其它金融資產一樣,房產價值也有客觀衡量指標,比如房價與房租比。下面的圖表來自《經濟學人》,這份圖表比較了全球各地有代表性的房地產市場的房價與房租比,相信這份圖表能夠告訴你哪些房產市場過熱(正值),哪些過冷(負值)。 房產中介會告訴我們每個市場都是不同的,但他們都有著三個相同點。 首先,每個過熱的樓市背後都有中國富人的身影。除低利率外,全球價格最昂貴房地產市場還有一個共同之處:來自中國的華僑。溫哥華、香港、新加坡和悉尼都是中國富人最歡迎的轉移資產場。他們的到來導致這些地區的房價衝到了天上。 其次,房地產泡沫的破滅需要時間。在美國和愛爾蘭,在經歷為期十年的繁榮與衰退周期後,房價目前低於合理價值。但西班牙和英國的房價仍有很大的下跌空間。殭屍銀行通常不願確認房貸壞賬損失,相當於在苦苦支撐房價,但現實最終一定會佔上風。房產泡沫破滅得越早,房事與建設就會越早開始復甦。 第三,樓市復甦可能需要更長時間。在二十年前,東京皇宮的土地價值超過了加州所有土地價值的總和。值得注意的是,壞的宏觀政策會帶來持久的傷害。長期緊縮的貨幣政策使日本房價冬眠了數十年。 加拿大目前正在試圖低調處理泡沫問題,具體方法是維持低利率,但讓抵押貸款更難以獲得。加拿大希望通過這種方法讓房價緩慢下跌,而不是觸發惡性循環。在最好情況下,房價表面上並沒有跌,wj但漲幅低於通貨膨脹率,這樣,從長遠看,房價實際是下跌的,但家庭的凈資產並不會突然縮水。 雖然這種辦法有個加拿大名稱叫做“宏觀謹慎調控(macroprudential regulation)”,但其實並非獨特,中國人幾年前就這麼做了。 在未來對抗樓市泡沫戰爭中,讓我們希望這種方法能夠奏效。(明煜) |

加拿大 溫哥華 中國城 China town

溫哥華 加拿大 Canada

|

|

加拿大的房市泡沫看來將要破裂

Canadian housing bubble looks ripe for popping Trend of rising prices and rising debt cannot be sustained. By: Adam Peterson Published on Sun Jul 14, 2013 Housing in Canada is unaffordable. International experts are unequivocal in their concern, and Canadian lawmakers are taking measures to deflate slowly rather than crash. Ironically, only Canadian homebuyers seem to think the market is sustainable. Sale prices are still rising. So when does it all start to unwind? Right about now. Since the Great Recession, the Canadian economic model has basked in international reverence for its conservative banks and rich commodity sector. So when Wall Street rumblings about a Canadian housing bubble started becoming louder about a year ago, as a card-carrying Canadian, I took notice. Over the last year, the “short Canada” thesis on Wall Street has evolved from a contrarian sidebar into a growing chorus. The Economist recently wrote that Canadian housing looks “particularly vulnerable” because of unsustainably high home prices compared to rents and incomes. The OECD expressed the same concern. Steve Eisman, a private investor profiled in The Big Short for shorting the U.S. housing market, recently presented several ways to short Canada. Even Paul Krugman, a fan of Canada’s economic and political backbone, recently published his concerns about Canadian home prices and household debt. Robert Shiller, the economist who predicted the collapse of the U.S. housing market, believes Canada could already be experiencing the correction that happened in the United States, only “in slow motion.” Canadian lawmakers and institutional stakeholders have taken notice and are positioning themselves defensively. The finance minister, the Bank of Canada and CMHC have tightened and continue to tighten lending standards to “cool” the housing market. CIBC shuttered its mortgage broker lending arm, FirstLine, and is considering selling its mortgage broker franchisor, Mortgage Center Canada. Those closest to the industry are pulling back on the reins. Coincidence? There are two primary issues: ● Home prices are so high relative to incomes that average households are very vulnerable to rate or income movements. ● Housing is such a big part of the Canadian economy that any small shift can be problematic. In Toronto, the median income is around $73,000, according to Demographia. The median home price is $455,000. After coming up with a 20-per-cent down payment, a “median” mortgagor would be on the hook for $22,200 annually, even at a 3.5-per-cent mortgage rate (which has to go up). If we include other housing costs (real estate taxes, maintenance, insurance, etc.), costs climb to $30,000 every year. Throw in cable, cellphones, groceries and Internet, and the family budget gets quite thin, quite fast. What happens when rates hit 5 per cent, or 8 per cent? My gravest concern is that Canada is fast approaching a 5:1 home-price-to-income ratio, a benchmark achieved by the U.S. at the peak in 2006. Since the correction, the U.S. ratio now hovers at approximately 3:1. To compound the problem, household debt in Canada has breached 150 per cent of income and continues in the wrong direction; households are not cushioned against a blow. Housing is big business in Canada, making up 19 per cent of GDP. A slowdown in housing production can be very hurtful and job losses can be severe. Furthermore, CMHC guaranties $600 billion worth of Canadian mortgages, the equivalent of the entire Canadian federal debt. A rise in mortgage delinquencies could be debilitating. I believe we are witnessing the crash right now in, as Robert Schiller put it, “slow motion.” In most major Canadian markets there is an increase in listings and decrease in sales (even though prices are still somehow rising). The Bank of Canada recently voiced strong concern over the number of unsold highrise units in Toronto, and how a housing correction could have a severe spillover to income and employment. Lawmakers appear to be facing the problem head on. The trick will be allowing home prices to glide down while combating the accompanying job and economic losses that a housing correction entails. Artificially low interest rates helped inflate this asset bubble and now present a Catch-22: raising rates in order to cool the housing market could push many homeowners into default (yet another lesson about the dangers of low interest rate environments). Although housing corrections are brutal, Canada could handle its correction in a more orderly manner because: It will (hopefully) not be accompanied by a meltdown in global credit. The system is not as fraught with fraud and the complications of securitization. The banking industry is far more consolidated and co-ordinated with the central bank. Lawmakers see it coming more clearly. Orderliness, however, does not compensate for the loss of jobs, home equity and consumer confidence that a housing correction brings. The Bank of Canada’s new leader, Stephen Poloz, has stated that for balanced and sustained economic growth Canada needs to focus on corporate capital expenditure and higher exports. I agree. That will drive higher wages and more diverse sources of economic output over time, but the pivot will take time, patience and creativity. In the meantime, the housing market is flashing red. Adam Peterson is a residential real estate investor with a New York investment firm. |